World reserve currency status is critical to the United States. It creates savings for the country because it causes U.S. interest rates to be lower than they otherwise would be. In turn, American consumers benefit from lower interest rates by getting lower mortgage interest rates. Lower-income households particularly benefit since they are typically much more leveraged than higher-income households, as documented in Amir Sufi and Atif Mian's 2014 book, House of Debt. Having higher household debt-to-GDP ratios means that the poor get to pay much lower interest payments than they otherwise would.

There have been many premature takes amid the China-Brazil announcement to no longer trade using U.S. dollars (USD), calling this the end of dollar dominance. While we may be at the beginning of a multi-polar world currency regime it is still very early and unclear what other countries would be winners from such de-dollarization. Further, many factors from inflation to geopolitics will determine the extent of the change.

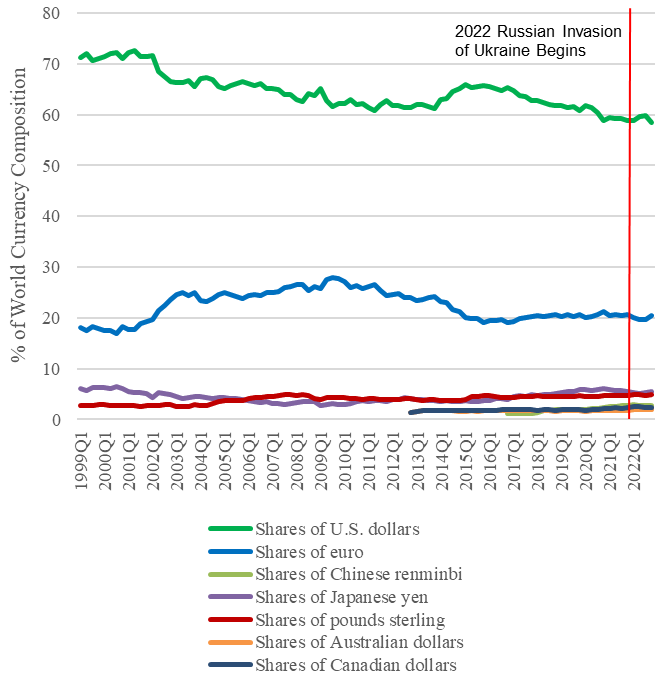

In June, the IMF released the Official Foreign Exchange Reserves (COFER) data: the USD share of world reserves decreased to 58.4 percent in the fourth quarter of 2022, the lowest level for the U.S. dollar since Russia invaded Ukraine in 2022. Could this be the start of declining dollar dominance amid geopolitical realignment?

Central Bank Foreign Exchange Reserve Shares By Currency (1999-2022)

Some short-run variation reflects changes in bilateral exchange rates—e.g., how many dollars you get for one euro—and central bank foreign exchange reserve managers being slow to rebalance. The USD exchange rate massively sold-off in the fourth quarter of 2022. Nonetheless, despite the rise in US dollar bilateral exchange rates toward the end of 2022, the USD share of world central bank currency reserves has been lower since Russia's invasion of Ukraine began.

Overstating the rise of the RMB

Arguably, coordination between central banks is what maintains U.S. dollar dominance today. Some of this coordination equilibrium may be shifting slightly away from the dollar amid the geopolitical uncertainty of Russia's Ukraine invasion and inflation. Some central banks, like the Bank of Israel, have announced moving out of U.S. dollar reserves. However, rather than shifting only to the Chinese yuan (renminbi or RMB), the Bank of Israel shifted to other currencies like the British pound, Japanese yen, Canadian dollar, Australian dollar, and New Zealand dollar. So the narrative around a rising Chinese yuan and falling U.S. dollar seems somewhat flawed.

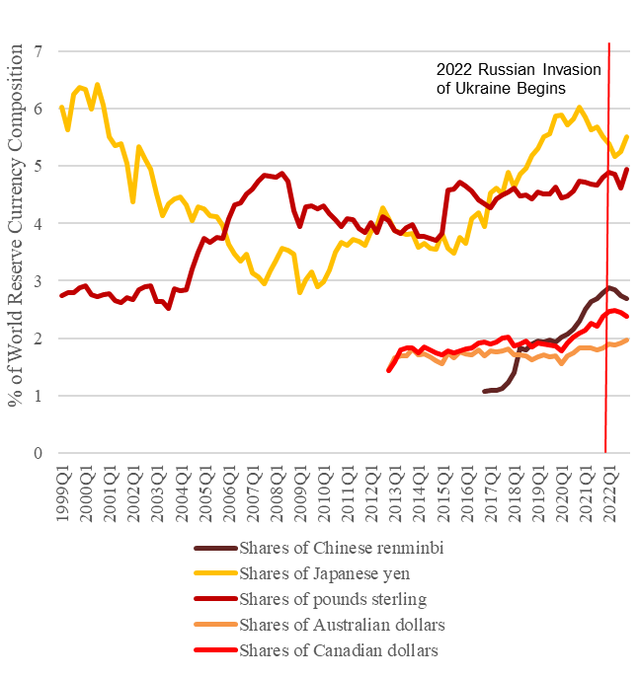

Central Bank Foreign Exchange Reserve Shares By Currency For Non-Traditional Reserve Currencies (1999-2022)

Interestingly, the pound and yen have benefited the most since the 2022 Russian invasion. They have seen the largest overall increases in shares of world central bank foreign exchange reserves while the renminbi share has been declining. (Caveat: this data preceded the recent China-Brazil business forum in Beijing.)

Inflation and the dominant currency in central bank reserves

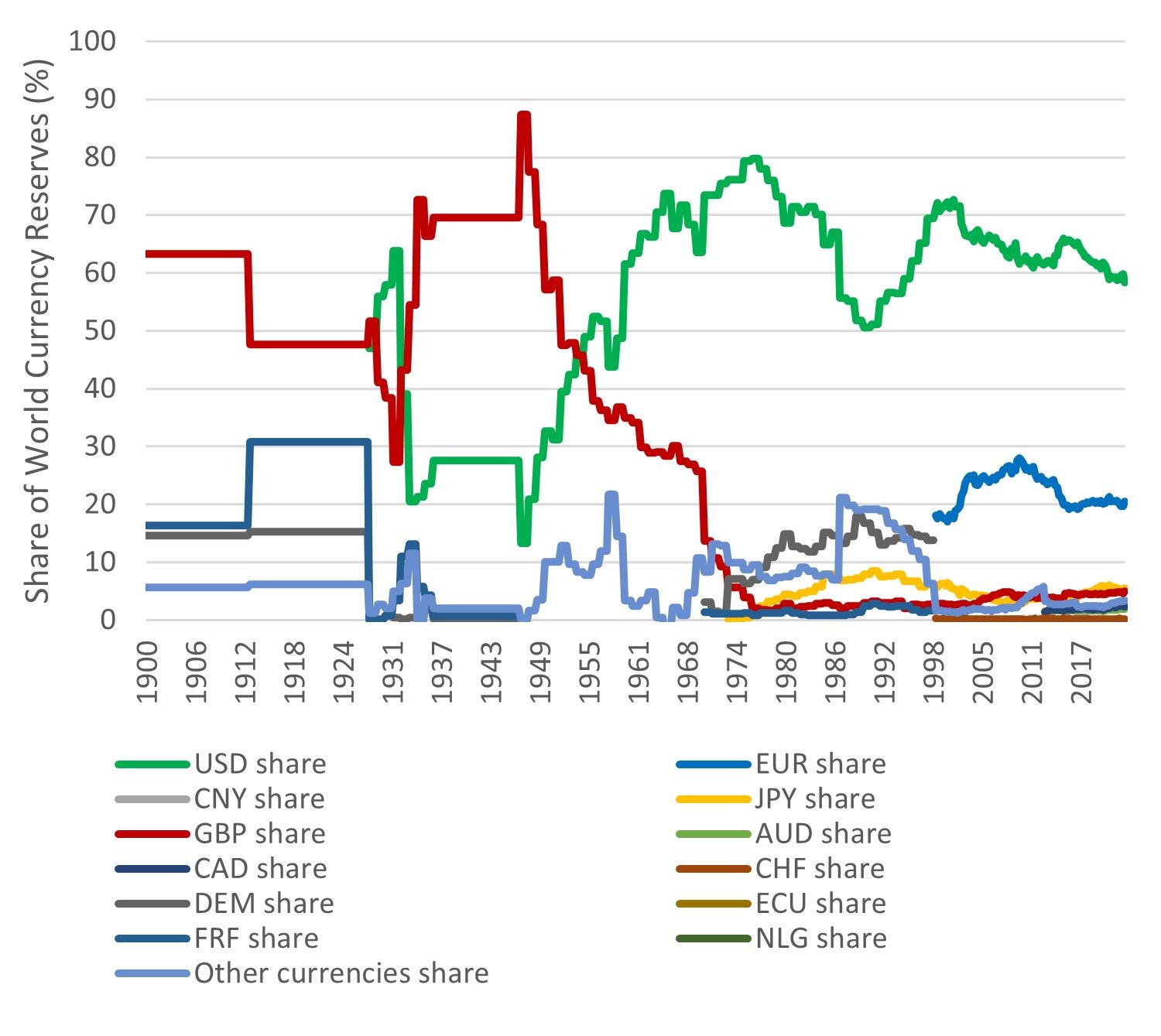

The real question is whether or not the U.S. dollar is experiencing the beginning of a de-dollarization process, much like the British pound experienced in the early 20th century during World War II.

In the mid-1970s, the dollar represented over 80 percent of world central bank foreign exchange reserves. But amid the high inflation of the late 70s and the breakdown of the Bretton Woods system, its share fell to 50 percent. Once inflation was brought under control in the 1990s with the advent of central bank inflation targeting, the dollar regained its role in the international finance system and represented over 70 percent of world central bank foreign exchange reserves again by the close of the decade.

But inflation has once again returned and the dollar share of world central bank foreign exchange reserves have fallen below 60 percent since 2021. To be sure, shifting to a different world currency regime usually takes considerable time. Sudden shocks do happen, but no such shock seems likely on the current horizon.

Central Bank Foreign Exchange Reserve Shares By Currency (1900–2022)

World reserve currency shares aren't the only indicators of the extent of dollarization and reserve currency status. As of 2022, nearly 90 percent of all foreign exchange transactions still involve the dollar as one of the transaction’s currency pairs, which has actually increased in the last decade.

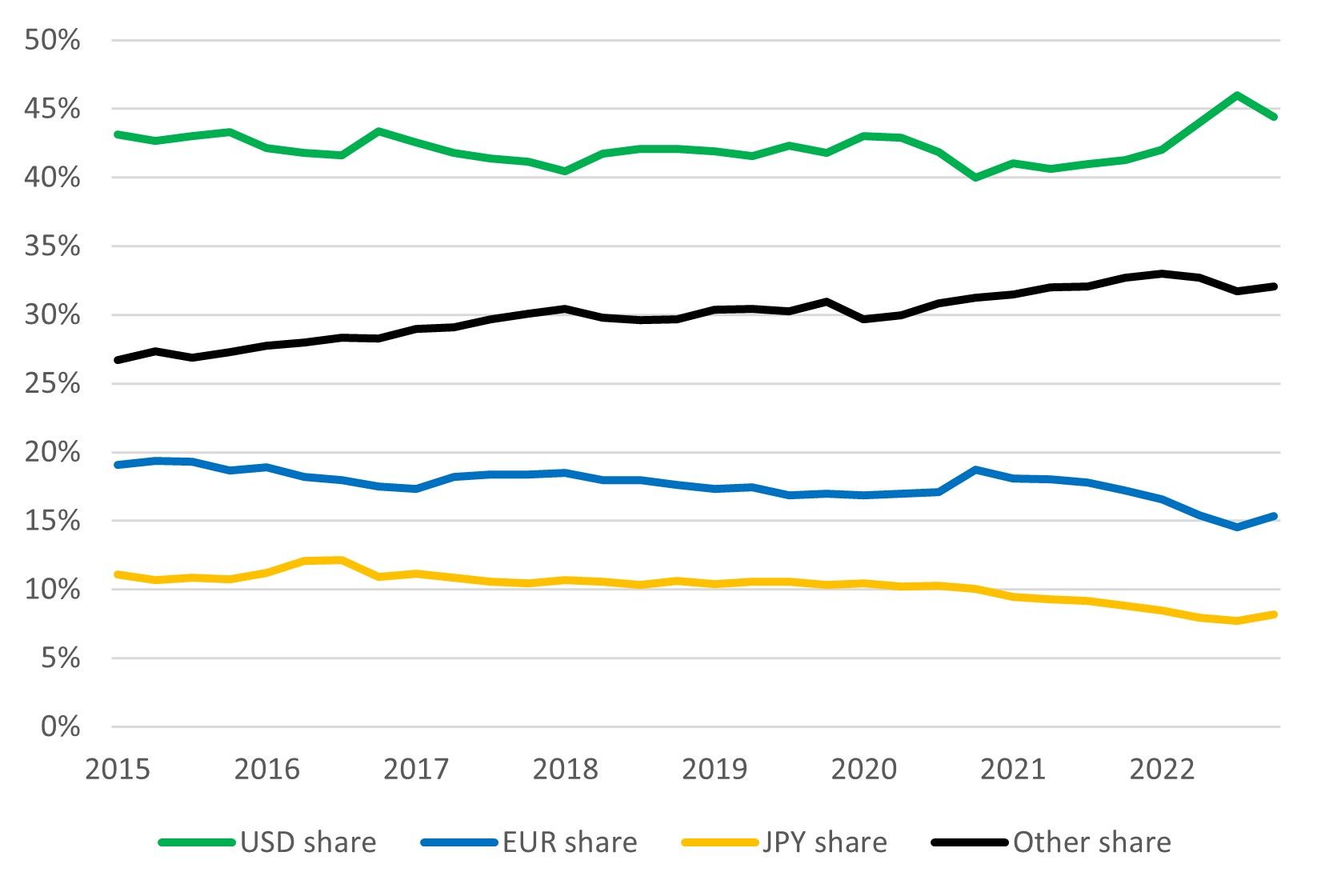

In addition, approximately 45 percent of global debt securities are denominated in the U.S. dollar, suggesting that the dollar is still largely the most popular global choice of currency domination for debt issuance across firms and governments.

Currency Denomination of Global Debt Securities (2015–2023)

The denomination of currency in trade flows matters as well. While the data we have on currency choice in trade invoicing is limited since the 2020 COVID-19 pandemic and 2022 Russian invasion of Ukraine, there is good reason to believe the dollar is still doing fine by this metric.

The extent to which the international financial system will continue to remain dollar-centric in the long run or further diversify into other international currencies remains to be seen. Whether the Federal Reserve can control and reduce inflation in the coming decade and whether geopolitics will stabilize will likely be the critical determining factors.